Vanik was a trailblazer of innovative financial instruments when it issued Sri Lanka’s first listed debenture twenty years ago. The company was decades ahead of its time and overconfidence led to overleveraging. Its star quickly burned out.

The grip on the artificial wood flooring is weak, Justin Meegoda, the Chief Executive of Vanik Incorporation, would’ve figured when he visited the Central Bank Governor’s new office in 1999, months after it was moved to a new wing of the headquarters building. A former Central Banker, Meegoda would have been familiar with the bank’s lay out from his years there in the 1970’s and found the new headquarters opulent. But the weak grip of leather shoes on smooth wood-like flooring would’ve forced him to concentrate on his strides.

Meegoda’s company was in crisis. Two years earlier, high-flying Vanik had acquired tea holding group Forbes Ceylon for Rs2.5 billion, Sri Lanka’s largest acquisition. But things had soon begun to unravel. In a bidding war with Asia Capital, Vanik had grossly overpaid for Forbes. When world tea prices crashed the a few months later, Forbes recorded a massive loss.

Forbes had been the culmination of a massive shopping spree by Vanik on borrowed money over the years. Even before the acquisition, Vanik’s borrowings had been so huge that its interest payments on them were more than half its turnover in 1996. The Forbes loss came on top of this, pulling the Vanik group into the red for the first time in its audacious six-year history. The news sent tremors through the industry, and there was a run on the money and capital market investments the public had with Vanik. In 1999 alone, the exodus of funds topped Rs4 billion.

Meegoda knew A S Jayawardena personally, but on this day in 1999, he visited the Central Bank Governor’s office in an official capacity on behalf of thousands of Vanik’s debt and equity holders. Vanik’s money was fully invested, which led to delays in refunding investors, increasing the fears swirling in the market.

In its short history, Vanik had introduced innovative financial instruments. If it was unable to repay its debt holders, the impact on the fledgling debt market would be significant. Meegoda wanted the Governor to tide over the cash-strapped firm with a Rs500 million Central Bank loan or to request a consortium of banks to provide it.

Jayawardena saw no reason to assist.

Since Vanik wasn’t a licensed commercial bank, the Central Bank had no obligation to help, he said. In the following days, the Central Bank began to check with commercial banks about their exposure to Vanik. Banks became jittery and froze the company’s facilities. What Meegoda saw as Vanik’s potential saviour had crystalized the crisis.

Sixteen years later, Meegoda is still trying to resurrect Vanik from a cramped office on Colombo’s leafy Flower Road. He’s now almost 70. “My family pushes me to give up,” he says. “But I have an obligation to our shareholders and creditors. I’ve never been tempted to give up.”

Pioneers are usually larger-than-life figures who venture into unchartered territory and alter the future. In business, they introduce new products or upend old ways of operating, and sometimes revolutionize whole industries. But not all pioneers find success. Great ideas need to meet the right economic climate and resonate with markets to succeed. Sometimes pioneers have to watch forces beyond their control obliterate their dreams.

Pioneers are usually larger-than-life figures who venture into unchartered territory and alter the future. In business, they introduce new products or upend old ways of operating, and sometimes revolutionize whole industries. But not all pioneers find success. Great ideas need to meet the right economic climate and resonate with markets to succeed. Sometimes pioneers have to watch forces beyond their control obliterate their dreams.

Justin Meegoda is one such pioneer.

In 1993, four Sri Lankan banking professionals launched an investment bank. They named it Vanik, meaning “merchant” in Sanskrit. Investment banks were a revolutionary concept in Sri Lanka, though they had been long established in rich countries. Moreover, no one in Sri Lanka had been bold enough to undertake such an audacious venture without sponsorship from the government or a corporate group. Vanik’s first office was a modest rented space with a borrowed computer and rented furniture. Its founders invested Rs10 million and, at an oversubscribed IPO, it raised Rs280 million.

Sri Lanka’s capital markets were rather unsophisticated, and most people wouldn’t have seen the need for an ambitious investment bank. But the Vanik founders’ vision was built on possibilities. Sri Lanka’s economy was full of promise, and the venture felt right for Justin Meegoda and his partners.

Sri Lanka’s opening for foreign trade in the late 1970’s had transformed the economy and the financial markets had grown. Even President Ranasinghe Premadasa’s assassination in 1993 didn’t deter the Vanik founders’ optimism. They expected a new parliament to prioritize public enterprise reform and for private firms to list on the stock exchange. Vanik was established to capitalize on these opportunities, especially those stemming from the capital market such as managing public issues of stock.

“We thought we could do something new,” recalls Meegoda. “We didn’t have much money. What we had was good track records.” After his years at the Central Bank, Meegoda had been part of NDB’s founding management team and then the first Managing Director of Bank of Ceylon’s investment banking subsidiary Merchant Bank of Sri Lanka. The other founders Abaya Wijeratne and Bhatiya Amarakoon had worked at NDB with Meegoda, while Sisira Jayasinghe had been at Merchant Bank.

Investment bankers abroad offer specialized skills around banking and capital markets. Often, in places like the US, investment banks specialize within sectors, dealing only with tech companies or just real estate and so forth. But this model wouldn’t work in Sri Lanka’s tiny capital market. Vanik also realised that this tiny size would make it difficult to find buyers for acquired companies.

Investment bankers abroad offer specialized skills around banking and capital markets. Often, in places like the US, investment banks specialize within sectors, dealing only with tech companies or just real estate and so forth. But this model wouldn’t work in Sri Lanka’s tiny capital market. Vanik also realised that this tiny size would make it difficult to find buyers for acquired companies.

In response, Vanik developed its own investment banking model, blending fee-based activities with fund-based activities. In addition to investment banking activities like underwriting and managing new share issues, Vanik also set up a leasing unit and pursued trade financing.

In 1994, Vanik declared a rights is sue of one share for every four shares, pioneering the concept in Sri Lanka. Share warrants give shareholders the option to obtain shares in the future index change for the warrants, either free of charge or at a specified discounted rate. Since a warrant is quoted, a shareholder

can also sell it in the market. That year, Vanik similarly issued Lease Securitization Certificates to the value of Rs100 million, again for the first time in Sri Lanka. This asset-backed security is secured by a collection of leases given by the company; their value is derived from the receivables owed on the leases.

Vanik also introduced leveraged buyouts. In the textbook model, companies use one of two ways to acquire another company. In the first, a company borrows money to meet the cost of acquiring the other entity and then uses the acquired company’s cash or other assets to pay off this debt. In the second, a company first buys a controlling interest in the other company and then uses the cash inside it to buy up the rest of the shares. Leveraged buyouts allow companies to make large acquisitions without committing their own capital. But Sri Lanka’s old Companies Act didn’t allow either of these, as it prohibited firms assisting third parties to purchase their own shares. But Vanik found a way around this without contravening the Companies Act.

As the financial advisor to Pakistani company Tawakkal, a bidder for government-owned Puttlam Cement, Vanik figured how to use leverage in a privatization. It used a system Meegoda had first utilized to buy out Kelani Tyres when he was Managing Director of Merchant Bank.

Few understood a leveraged buyout; the Puttlam Cement buyout stirred up controversy and was debated in parliament. Foreign Minister Lakshman Kadirgamar said that the method was too sophisticated for a market in Sri Lanka’s state of development.

In 1996, Vanik issued Sri Lanka’s first debenture, raising Rs150 million and securing a stable source of funding for itself. Debentures are now floated frequently by Sri Lankan firms, but two decades ago it too became controversial. “Many banks, that now issue debentures themselves, complained to the Central Bank that we were raising deposits although we weren’t a deposit-taking institution,” recalls Meegoda.

In 1996, Vanik issued Sri Lanka’s first debenture, raising Rs150 million and securing a stable source of funding for itself. Debentures are now floated frequently by Sri Lankan firms, but two decades ago it too became controversial. “Many banks, that now issue debentures themselves, complained to the Central Bank that we were raising deposits although we weren’t a deposit-taking institution,” recalls Meegoda.

Meegoda explained to the Central Bank that debentures weren’t deposits, but debt. The Central Bank understood. For several years, the Colombo Stock Exchange’s total debt security capitalization was Vanik’s liabilities.

Vanik became the market leader in managing public share issues. A fully owned subsidiary Vanik Corporate Services managed 24 public share issues (raising Rs3.64 billion) of a total 69 issues raising Rs9.86 billion during Vanik’s first nine years as an investment bank.

Vanik also mobilized significant foreign capital, both debt and equity, for privatization and IPOs of large private companies. The company estimates it brought Rs1.1 billion in funds into the country during its first six years.

In spite of innovation, Vanik’s profits were relatively meagre. The country’s financial services business was simply too weak for a company to survive on these services alone. Moreover, since the Kumaratunga government’s election in 1994, the economy had been sputtering, with the intensifying war leading to high borrowing and high interest rates. Vanik wanted to expand into areas that would provide security against market volatility and economic downturns, and eyed asset-rich Forbes Ceylon. Unfortunately, this potential ladder out of trouble turned out to be quicksand, and Vanik never recovered from the post-acquisition trauma.

Over the years, Vanik had borrowed heavily to fund its acquisitions. Its interest payments on borrowings in 1996, even before the huge Forbes acquisition, were more than half its turnover. Investment banks abroad usually sell their acquisitions at a profit. But in small markets like Sri Lanka, investment banks tend to become holding companies because they don’t have buyers for these acquisitions. This was Vanik’s case. In 1996, Vanik had Rs4 billion in liabilities versus Rs5 billion in assets. The company was on a raging shopping spree, and it was buying on credit. Moreover, it was racking up debt at a time of volatile interest rates. It was a recipe for disaster, even before Forbes came on the scene.

Today Vanik’s liabilities total almost Rs2 billion. This includes half a billion each to banks and to cooperative banks; Rs170 million and Rs180 million to individuals and corporates, respectively – not just companies, but also associations and even places of worship – who hold money market borrowings; and Rs200 million to USAID due to a debenture the agency partly guaranteed in 1998.

Today Vanik’s liabilities total almost Rs2 billion. This includes half a billion each to banks and to cooperative banks; Rs170 million and Rs180 million to individuals and corporates, respectively – not just companies, but also associations and even places of worship – who hold money market borrowings; and Rs200 million to USAID due to a debenture the agency partly guaranteed in 1998.

Of a 15% unsecured debenture that Vanik issued in 1997 to buy Forbes, there’s still almost Rs350 million in capital outstanding, while on other debentures and bonds it owes Rs43 million.

Debt-holders still come to Vanik’s door. Recently, at a court hearing, the prosecution questioned Meegoda’s preferential treatment to some debtholders. Meegoda replied that, when individuals come to his office asking for Rs25,000 or Rs50,000 to pay formedical expenses, h e cannot turn them away. The judge just listened to the exchange.

Today, Vanik is barely above water and has four employees, plus a driver and a cleaner. The legal officer works on a retainer basis.

Vanik has several active subsidiaries including Forbes Ceylon, which acts as the holding company for other subsidiaries such as LM&A Insurance Brokers & Consultants and Vanik’s travel agency Tour East (Lanka). Each of these employs about 12 to 14 heads. The group also owns a tea plantation. Forbes Ceylon is just a holding company now; all its assets have been sold.

Vanik’s assets today are its 5.5 million Softlogic Finance shares and one million Softlogic Capital shares. At the current market prices, these holdings are worth over Rs300 million. Vanik also had 2.6 million shares in Softlogic Credit, which was sold to Laugfs Capital, which is being merged with savings bank CDB. Vanik will receive CDB shares for its holding. Vanik has holdings in these firms because these used to be its subsidiaries, but its controlling interests were sold during the peak of its crisis.

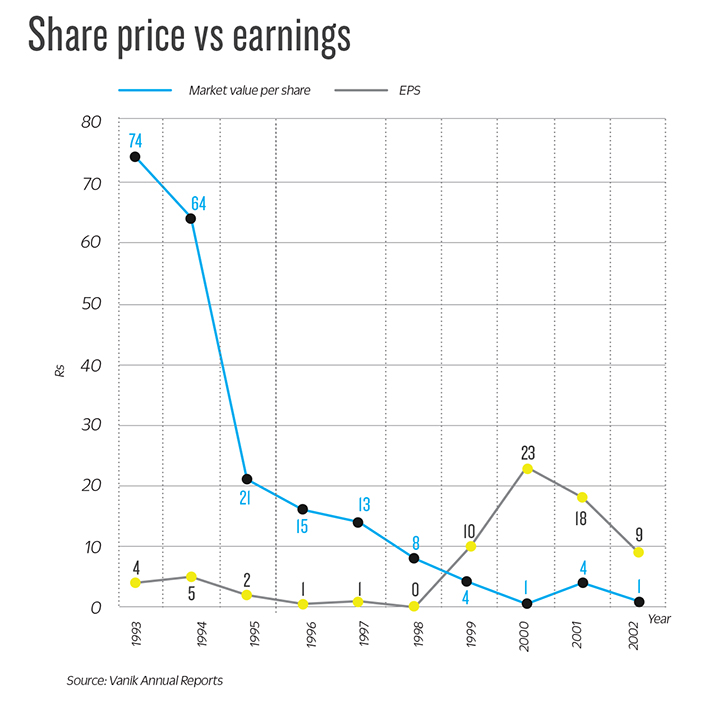

Incorporated in late 1992, Vanik rode the successful wave of merchant banking’s newness in Sri Lanka and grew rapidly in its first six years. After its oversubscribed IPO, it made Rs52 million profit in its first year of operation and almost tripled this the following year. During this year, it acquired a controlling interest in Sri Lanka’s then third-largest finance company, LB Finance, as well as in Prestige Property Development, a BOI project. Vanik mobilized over Rs2 billion in 1994 alone to finance acquisitions and support the government’s public enterprise reform efforts.

In 1995, a second rights issue was also oversubscribed. The company became more ambitious. It began looking at expanding overseas, signing an agreement to set up Vanik Bangladesh, though it would take two more years to establish the business due to delays by Sri Lanka’s Central Bank. Vanik also purchased 240 perches of prime land on Galle Road to build an office complex, and its subsidiary Prestige Property development signed an agreement with Kinhill Engineering in Australia to manage construction. It was not yet three full years since the company had been incorporated.

But Vanik’s profit never grew parallel to its ambition. Vanik was affected by a stuttering economy and the new government’s lack of commitment to open markets. Strikes were frequent in factories, and the war intensified. Military hardware costs and subsidies weakened public finance. Naturally, interest rates rose as the government borrowed more. The tanking stock market reduced trading opportunities and capital market fee income dried up, forcing Vanik to expand its fund-based activities.

But Vanik’s profit never grew parallel to its ambition. Vanik was affected by a stuttering economy and the new government’s lack of commitment to open markets. Strikes were frequent in factories, and the war intensified. Military hardware costs and subsidies weakened public finance. Naturally, interest rates rose as the government borrowed more. The tanking stock market reduced trading opportunities and capital market fee income dried up, forcing Vanik to expand its fund-based activities.

Vanik increased its stake in LB Finance to 89% and in Prestige Property Development to 100%. By the end of 1996, the company had infused over Rs330 million in its office construction project of Rs132 million in equity and Rs200 million in debt. At this point, the company’s net book value exceeded a billion. “Most giants in the financial industry were scared,” says a former senior employee of Vanik’s leasing unit, who declined to be named. “Friends who worked for other institutions at the time said they were losing clients, even in leasing. They were upset.”

In 1996, a bomb damaged the Central Bank and a drought led to electricity shortage. The war intensified. Inflation kept rising. By yearend, the All Share Price Index (ASPI) had dipped to a four-year low of 603 points. Vanik decided to curtail growth and consolidate. It reduced lending at LB Finance, and made loan recoveries the focus. It divested holdings in Puttlam Cement and Colombo Communications, which operated three radio stations.

Meegoda and his management team made it a point to hire young graduates from local universities. “In the corporate sector, there’s still a myth that they’re unemployable,” he says. “I proved this wrong. They turned out to be very good. They became our backbone.”

The firm became a university for Sri Lanka’s capital markets.

The distinguished roll call of alumni includes Ajit Fernando, Founder and Chief Executive of Capital Alliance Group; Dharshan Perera, Chief Executive of NDB Investment Bank; Mayura Fernando, a former Chief Executive of Laugfs Capital; Ranil Pathirana, who heads the Hirdaramani Group; Nalin Wijekoon, Chief Executive of Softlogic Finance; and Keerthi Wijeratne, Head of Leasing at Cargills Bank.

“What I learned at Vanik is one of the success factors in my life,” says Perera, who joined Vanik’s factoring unit in early 1996. “Those who worked at Vanik were given the opportunity to learn. Even though Vanik isn’t around, those who worked there are now everywhere.”

When Vanik realized that Sri Lanka’s financial services business was too weak for the company to survive on these services alone, it began to diversify. In 1997, it inaugurated subsidiary Vanik Insurance Brokers and bought a 14.4% stake in Pan Asia Bank.

At the end of that year, Vanik acquired 125-year-old tea broker Forbes Ceylon for Rs2.5 billion. Forbes’ asset base was twice the size of Vanik’s. The latter saw cash-rich Forbes’ diversification and large assets as a base with which Vanik could weather the weak financial services business. It would help Vanik expand into new areas and provide security against market volatility and economic downturns.

By the end of 1997, Vanik had metamorphosed from an investment bank into a 33-company conglomerate operating in financial services, plantations, plantation services, travel and tourism, real estate and food products. The group’s assets were at Rs13.5 billion, a three-fold increase from a year before. That year, profit tripled. This was supported by the Sri Lankan economy bouncing back, recording over 6% growth. Inflation had declined to under 10% from 15% a year earlier. Lower interest rates and liquidity pushed the ASPI over 800 points.

Companies usually acquire other companies in the same industry, either vertically for a related business or horizontally for a competitor. The Forbes acquisition was neither. It was a buyout of a large, diversified group with businesses in areas in which Vanik had no experience: tea and leisure. An acquisition of this scale was risky, but analysis showed it as a good buy.

But things didn’t go as expected.

“Mr. Meegoda was an entrepreneur and always wanted to take risks,” says Perera. “But the environment at that time didn’t favour risk taking. Unfortunately, Vanik also made some bad decisions. Acquiring land to build its headquarters was one.”

“I think the acquisition was too big for Vanik,” says Perera about Forbes. Forbes’ management team left the company to set up tea broker Asia Siyaka – a company linked to Asia Capital – soon after the acquisition. Forbes lost 12% of its market share overnight.

Vanik followed its management autonomy pol icy with Forbes. In some ways, Vanik had no choice, as it had no tea broking expertise. “They were just operating on their own, and whoever we sent in from Vanik wasn’t able to maximize returns,” says Perera.

Soon after the Forbes acquisition, Vanik also bought a fifth of Watawala Plantations.

The former leasing employee believes it was a classing of all eggs in one basket. “They were investing short-term funds on acquisitions,” he says. “These were huge investments. Even one failure would have made a huge impact. The interest cost and the risk were huge. If it was a diverse portfolio with a lot of small investments, it wouldn’t have been a problem.”

The land for the head office had also been purchased on short-term funding, another fundamental mistake.

He also believes that Meegoda’s belief in people also contributed to the company’s troubles. “Justin Meegoda believes everyone is genuine,” he says, and adds that some employees of acquired companies took advantage of this and of the management autonomy Vanik allowed. Perera agrees that Meegoda’s second tier may have also lacked the experience to support his ambition.

There was more grief to come for Vanik. Global tea prices declined. Forbes was all tea; they did tea broking, and owned Kahawatte Plantations and stakes in other plantations, as well as a company that provided services to the tea industry such as fertilizer and storage. In 1998, Forbes made a massive loss.

“We thought we were experts in M&A,” says Meegoda. “We did meticulous financial analysis. It was a perfectly good buy. But we didn’t consider the macro risk. We were riding a wave.”

Sri Lankan stocks continued a downward slide, with the ASPI ending the year at an eight-year low. The business slowdown affected credit growth, and companies faced cash flow problems. At the end of the year, the Vanik group found itself in the red for the first time.

“A lot of people at that time weren’t very positive towards Vanik,” says Meegoda. “Perhaps it was jealousy, perhaps it was because these unknown people were doing well. They spread all kinds of rumours through the market.”

Fueled by the speculation, investors began to withdraw their investments in Vanik’s money market instruments and commercial papers. When this occurs in a bank, the Central Bank may step in with liquidity. Vanik didn’t have that kind of support, as the Governor made obvious to Meegoda at their meeting.

After the meeting, the Governor also sent a team of Central Bankers to monitor Vanik, and for almost two years there were two officers stationed in the office. The greatest damage to Vanik, however, was the Central Bank’s calls to commercial banks to check their exposure to Vanik. Since then, to this day, Vanik hasn’t received a single rupee in bank loans.

Eventually, a total of about Rs12 billion went out of the company. Vanik was able to recover and use a Rs3.5 billion leasing portfolio and a similar bills discounted portfolio to pay investors. “We did this without support from any bank,” says Meegoda. “Even a small shop needs an overdraft. I must thank God we survived somehow or the other. A lot of people thought Vanik would be finished.”

Eventually, a total of about Rs12 billion went out of the company. Vanik was able to recover and use a Rs3.5 billion leasing portfolio and a similar bills discounted portfolio to pay investors. “We did this without support from any bank,” says Meegoda. “Even a small shop needs an overdraft. I must thank God we survived somehow or the other. A lot of people thought Vanik would be finished.”

In its 1999 annual report, Vanik’s auditors Ernst & Young expressed doubt about the company’s ability to meet its obligations in the future unless its performance improved. They based this view on the company’s interest expenses on borrowings exceeding its income from fund-based activities by over Rs215 million, resulting in an operating loss of almost Rs270 million. Its net loss for the year was almost Rs700 million, while its assets fell by almost Rs650 million that year.

In 2000, Vanik’s liquidity crisis reached its peak. About Rs4 billion had to be made in repayments. The company encouraged staff to quit and over 100 of the 260-strong staff left. This almost halved the payroll cost.

Vanik sold most Forbes Group firms and a part of its lease portfolio, leading to a significant revenue decrease. The mushy economic circumstances were unhelpful. By year-end, the group reported its biggest-ever loss of Rs.1.8 billion, but almost 40% of this was due to doubtful debts and declines in its share portfolio value.

In 2000, the auditors repeated their reservations. They added that interest expenses on borrowings exceeded income from fund-based activities by half a billion rupees and liabilities exceeded assets by Rs1.5 billion.

“Vanik’s story is an incredible one, started by a man with a vision,” says Perera. “He was ahead of his time. Some of the new things he introduced weren’t understood. The market wasn’t ready. Also, the economic climate and the political situation weren’t conducive. If he had done some of these things now, it would’ve been different.”

In 2001, when it became obvious that the Central Bank wouldn’t help Vanik, the company put together a restructuring proposal for its creditors. Meegoda asked the banks to form a consortium to back Vanik by lending it a further Rs500 million to get through its crisis. “Even that might not have been necessary,” says Meegoda. “It would’ve been enough if the market knew the consortium was helping me.”

Then Chairman of People’s Bank Mano Tittawela agreed to lead the consortium and convened a meeting. As a co-guarantor of a debenture Vanik issued in late 1998, USAID was also involved in the restructuring proposal, sending a Washington, D.C. expert to help. Most of the banks agreed to the restructuring proposal, says Meegoda, but Bank of Ceylon declined. When the main state bank refused the proposal, all the others did so too. “It was a verysad situation,” says Meegoda. “If that hadn’t happened, it would’ve been a different story.”

In 2002, Vanik put forward a second restructuring proposal. The company owned a lot of assets, including 15% of Pan Asia Bank’s shares, 65% at LB Finance and 20% at Watawala Tea Plantations, as well as the 240-perch land on Galle Road. Since the market was depressed, Vanik wouldn’t have been able to obtain the best price in an asset sale. So the company proposed to the government to keep Vanik’s assets as a security and issue a longer-term treasury bond, which Vanik could discount in the market and raise funds. “The government didn’t have to put in any money,” explains Meegoda. “They would have had the assets as security, and I assured them that over the next ten years, they’d be able to realize much more than that and I could get the surplus as well.”

After presenting this proposal, Meegoda met with then Prime Minister Ranil Wickramasinghe, who gave the proposal to Treasury Secretary Charitha Ratwatte Snr., but it didn’t go any further. Meegoda met with the Central Bank Governor again, but Jayawardena questioned the value of the assets.

“I asked for only Rs900 million,” Meegoda says. “But they didn’t even look at it. The assets were worth a lot. Later, that land alone was worth that much. At least if someone had looked at my proposal, but nobody was prepared to do that.”

Some of these assets had been placed as security with Vanik’s banks, and Seylan Bank and Bank of Ceylon sold them in that depressed market. The Pan Asia Bank shares were sold at just Rs5. “I almost begged them not to dothat,” Meegoda says. “I told them to just keep them, that later they’d be able to recover their money.” The LB Finance shares were also sold at just Rs11 and the Watawala shares at Rs11. Although Meegoda met with the banks and opposed the sales, the banks used Power of Parate Execution to sell them. The banks were unable to recover the full amount they had lent, while Vanik lost many of its assets.

Vanik also lost its 240-perch Galle Road property to DFCC, a commercial bank. At that time, the land was valued at Rs1 million per perch, but by the time the bank sold it a year or two later, the price had gone past Rs2 million. The bank not only recovered the money, but the buyer eventually sold the land to its present owners at Rs5 to Rs6 million per perch. “Just that would’ve been enough,” says Meegoda. “I was a victim of all these banks. They can’t look at anything innovatively. They just go with the standard practice of selling the security and recovering what they can.”

When Meegoda realized that neither the government nor the banks would help him, he went to courts in 2006 to ask it to call a meeting of the creditors to present a new restructuring proposal.

When Meegoda realized that neither the government nor the banks would help him, he went to courts in 2006 to ask it to call a meeting of the creditors to present a new restructuring proposal.

In the proposal, Vanik requested all of its institutional creditors to convert part of the debt to equity, with the remainder to be paid over three years, all accrued interest waived and new interest also paid in equity. Similarly, Vanik requested the debenture holders and the money market instrument holders to waive all interest, with the amount to be paid over three years at 12% interest. The proposal meant that the existing shareholders would take a hit by writing off 90% of their value.

More than 75% of the creditors and later the shareholders approved the proposal, which makes it binding on all the creditors under the Companies Act. But People’s Bank and Seylan Bank were opposed to it and filed cases to prevent restructuring, saying that, as banks, they couldn’t accept Vanik shares, as they weren’t allowed to invest in them. “They wouldn’t have been investing in shares; it was a recovery process. For instance, if a bank holds land as a security, a default results in them taking over the land. The bank isn’t in the business of selling real estate, but nevertheless it takes the land. Similarly, in this case, the banks could take the shares. But they couldn’t understand this simple thing, so they went to courts.”

The company presented to the courts that one creditor cannot stop a scheme that’s been approved by three-quarters of the creditors, but the courts allowed the cases to proceed.

Meanwhile, a Malaysian entity called the Public Bank filed a winding up case against Vanik to recover Rs5 million. After several years, the district court gave a winding up decision. At this point, Vanik terminated its restructuring plans, so the cases filed by People’s Bank and Seylan Bank were laid by.

Vanik appealed the winding up decision. The appeal consisted of a revision application and a final appeal. After about two and a half years, the courts rejected the revision application. The final appeal has now been pending for four years. In early May, there was another hearing, and it was again postponed because the judges had been changed yet again.

This winding up case has more or less tied Vanik’s hands. It cannot implement the restructuring proposal that had been approved by three-quarters of its creditors. “Since we put together this proposal, the market has changed, various things have happened, but I still believe that I can do a restructuring, of course with some modification,” says Meegoda. A court judgment in Vanik’s favour would imply that its restructuring proposal could be implemented.

If the restructuring plan had gone ahead, most of Vanik’s Rs2 billion debt would’ve been turned into equity and the balance, as well as the interest, paid over time. But instead, the company has been spending on legal fees. Meegoda estimates that the company has paid roughly Rs20 million in legal fees since 2006. Due to the winding up case, trading of Vanik shares has been suspended. With the court case hanging over Vanik, Meegoda says most companies are unwilling to hire its services. “Only people who know me personally use our services,” says Meegoda. Vanik’s hands are tied also when it comes to its assets. The company cannot sell its investments.

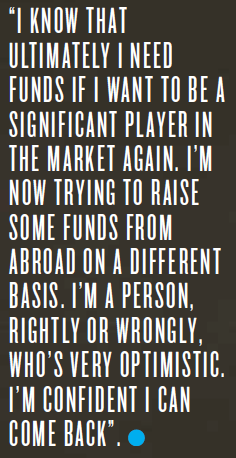

Meegoda says that Vanik does corporate finance projects and business evaluations, “jobs that come on and off ”. But mainly the company is waiting for a settlement to its court case. “I’ve lost faith in many of these things,” says Meegoda. “I know that ultimately I need funds if I want to be a significant player in the market again. I’m now trying to raise some funds from abroad on a different basis. I’m a person, rightly or wrongly, who’s very optimistic. I’m confident I can come back”.

Whether Vanik can do so, though, is up for debate. “I think it’s a bit too late now,” says Perera. “He’s been out of the market for about 15 years.”

“Justin Meegoda didn’t just run away from his challenges,” Perera adds. “He is genuine and is trying to resurrect the company. As a person, he had great qualities. He looked after his staff and took care of everyone.”

Meegoda is still optimistic about Vanik. “That’s why I’m here,” he says. He hasn’t drawn a salary for two to three years, although he puts in a full day at the office. He sometimes personally funds office expenses. “Not because of charity,” he says. “But because I feel 100% sure I’ll come back.”