Sri Lanka is now proceeding steadily into greater balance of payments pressure, with some mild signs of debt distress also emerging and in a twist not seen in the past, the Central Bank itself is getting increasingly into debt. Since the last column by Bellwether, the Treasury bill stock of the Central Bank, which is the key proxy for printing money and triggering balance of payments trouble has doubled.

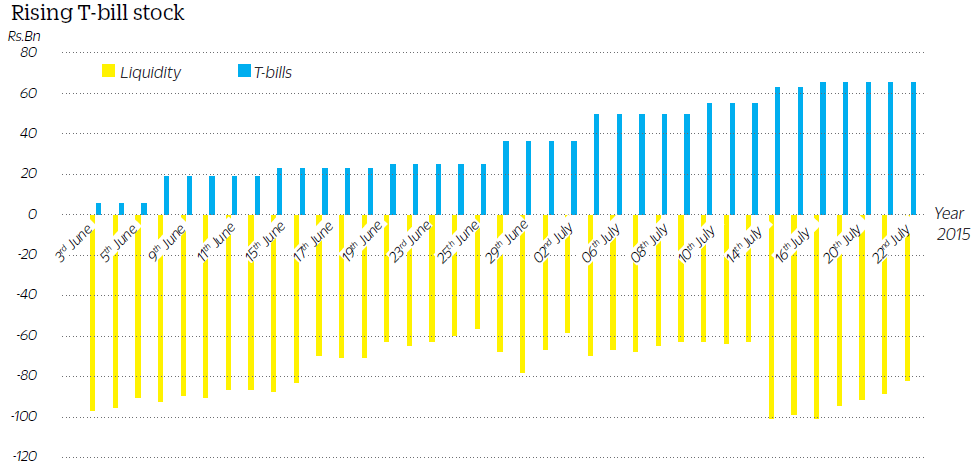

On June 01, the Treasury bill stock of the Central Bank was 5.4 billion rupees after terminating all term repos and selling down bills it had. The stock had climbed to 36.3 billion rupees by 30 June. By the last week of July, it had climbed to 65.9 billion rupees.

In June the Central Bank sold 506 million dollars to commercial banks to defend the currency, while buying only 15 million dollars according to official data. However currency purchases are under-reported due to exclusion of Treasury surrenders. The Central Bank had in fact been ‘acquiring’ Treasury bills in a roundabout way since the last quarter of 2014, but they did not show up in the data as a steady trend for several reasons.

The pre-June acquisitions happened mostly by terminating term repurchase deals. Under a term repurchase deal Treasury bills are temporarily sold to market participants in return for excess liquidity generated from dollars. When they are terminated the bills come back to the Central Bank and the liquidity is released. Some of the bills were also borrowed from the Employees Provident Fund, the balance sheet treatment of such transactions also seemed to be different.But now completely new Treasury bills are being bought anew and it can be unambiguously seen how the domestic assets of the Central Bank is climbing.

Turning Point

Turning Point

● One can argue about what exactly is a fully-fledged ‘BOP crisis’ as episodes of balance of payments pressure tends to intensify over time. But regardless of what stage of a crisis or otherwise a country is in, a central bank can pull out of the path at any time it wishes, by ending contradictory policy that is behind the problem. But in Sri Lanka and other ‘soft-pegged’ countries – where central banks repeatedly try to print money and try to control the exchange rate at the same time – policy corrections come only after a lot of reserves are lost and following advice from the International Monetary Fund and perhaps after a credit or outlook downgrade.

When a BOP pressure episode reaches ‘crisis’ proportions, the corrective medicine in terms of interest rate hikes and currency depreciation have to be harsher and the subsequent economic downturn and credit squeeze is worse, and the currency depreciation hurts ordinary people more.

Strictly speaking this columnist prefers to define the ‘crisis’ period as a time when the Central Bank is selling dollars to defend the currency and is then forced to inject liquidity to keep rates down, which is indicative of a vicious cycle of sterilized foreign exchange sales.

What is happening now is more of a straightforward monetizing of debt, where some money is printed ahead of the interventions, to maintain high levels of excess liquidity, artificially low interest rates and drive the banking system towards crisis point.

For example on July 02, the Treasury bills stock of the Central Bank went up from 36 billion rupees to 50 billion rupees and excess liquidity went up from 58 billion rupees to 70 billion rupees. By the following Friday liquidity was down to 62 billion rupees as dollars were sold, and then another 5.0 billion rupees of T-bills were acquired after that weeks’ bill auction.

Monetization

● This is straight forward monetization of debt, or printing money which is then hitting the BOP. On July 15, excess liquidity rose to 101.2 billion rupees, with some dollars being converted but the Treasury bill stock went up another notch to 63 billion rupees. This event coincided with a large rupee bond rollover, when some foreign investors appeared to have chosen not to roll-over their bonds at the same time as dollars were converted.

The 2011 crisis came despite the sale of a billion rupee bond in August 2012 because domestic credit growth was very high and it was eating up all the liquidity. A similar event was seen in July when excess liquidity rose to 101.2 billion rupees from 63 billion rupees when a dollar loan was converted on July 15, but liquidity was down to 83 billion by July 24, with interventions in forex markets.

While foreign borrowings does ease pressure on domestic credit markets, and can bring temporary relief, it cannot correct the underlying problem which is to do with excess consumption by the state through deficit spending and too low interest to curb consumption and generate enough deposits to feed the credit demand.

The 2011/2012 crisis was largely driven by credit taken to subsidize electricity and fuel. There was a drought and a rise in global commodity prices amid US quantity easing. The energy subsidies came on top of strong domestic private credit, but the central government budget itself was not in too much of a bad shape, because handouts were given through state enterprises by proxy.

This time the problem appears to be mainly state salary hikes and various subsidies which are given left and right directly by the state with global commodity prices coming down with US quantity easing ended and rate hikes on the horizon. The Ceylon Electricity Board is in fact making profits amid lower commodity prices and rainfall. But the advantage to the BOP from oil price falls have largely been taken away through price cuts in energy and also the subsidies given to tea and rubber farmers. Though international commodity prices are low, this time, rupee bond holders are pulling out. In the 2011/2012 crisis, they mostly stayed put and almost the entire problem was created by domestic credit.

Mild Debt Distress

Mild Debt Distress

● Government debt is gilt edged they say, because the government can always print money, when they are in debt distress. In fact this is what is happening.

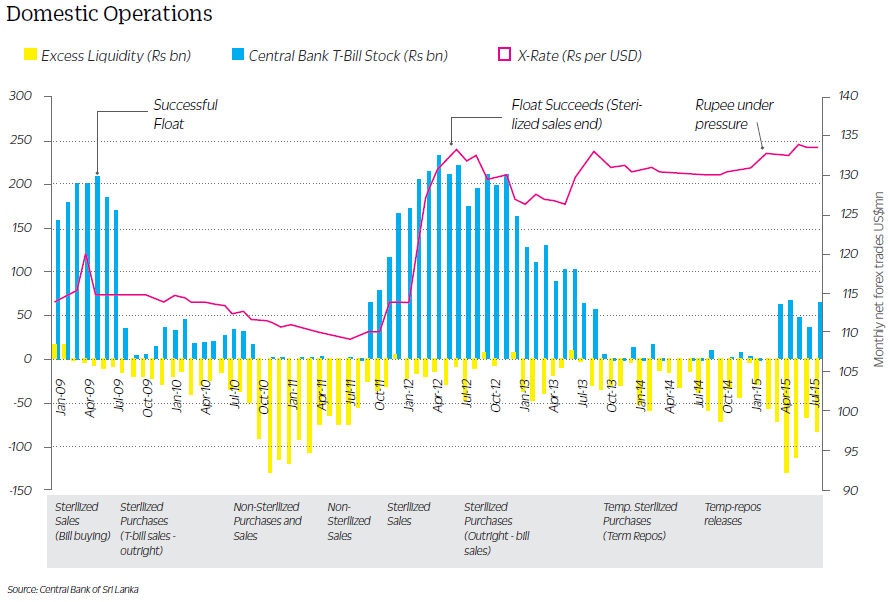

Foreign investors are steadily pulling out money from rupee bond markets, not in a panicky way but steadily. The Central Bank is absorbing the shock by refusing to raise rates and that is why the domestic assets of the Central Bank are rising. It was also happening before July, with the release of liquidity by ending term repo transactions, which shows that the condition is persistent.

In the past this happened from time to time, but the interest rates scenario was such that the bill could be sold down. In January for example a 500 million dollar bond was repaid without going to the market for rollover as a conscious decision and reserves were used. There is no harm in that, reserves should be used for contingencies.

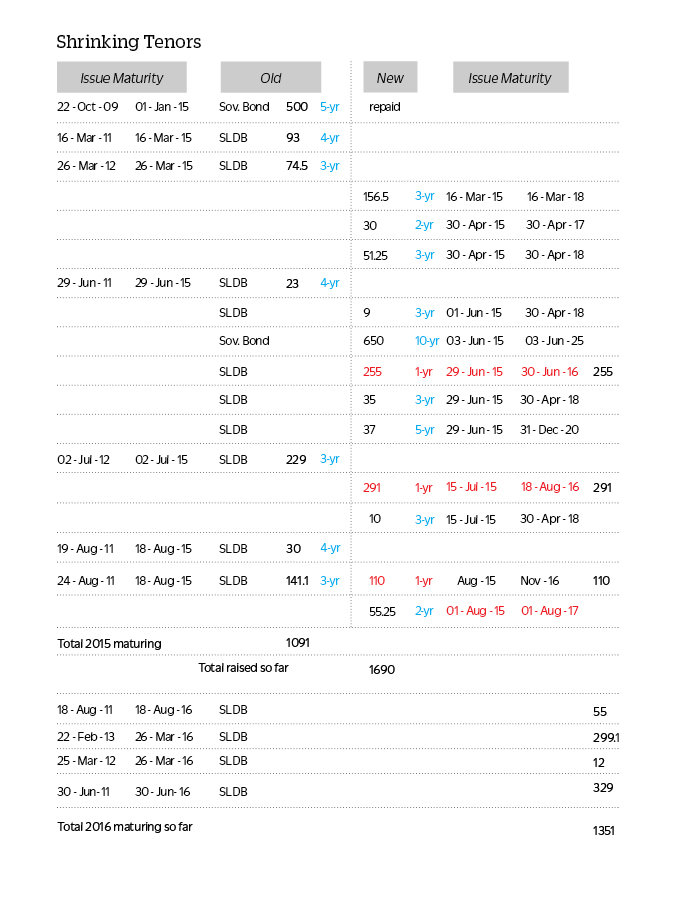

But in 2015 due to mis-management of excess liquidity in particular and low interest rates in general the Central Bank has not been able to recover lost reserves, and the underlying trend is persistent. The mild debt distress is also seen through another trend. Sri Lanka has been aggressively selling dollar bonds in the domestic market, but most of it had in fact been rollovers. But up to April Sri Lanka was rolling over debt comfortably.

In June a 650 million dollar sovereign bond was sold for 10-years at a reasonable yield. But the bond only bought 150 million dollars more that repaid a 5-year bond, and much less than the 1.5 billion dollars originally expected. In the floating rate market from June greater volumes of bonds were sold, but most of the new debt seem to be of a very short tenure of around a year.

On July 02, 229 million US dollars of 3-year bonds matured. But on July 15, only 10 million dollars of 3-year bond were sold. Another 291 million dollars were sold, but only in one year tenure bonds.This shows that Sri Lanka was not able to roll-over bonds for 3-year at least at the rates, authorities are comfortable with, so tenures are shrinking. It is well known that there is a lot of short term money in the Middle East but they are unwilling to go for two or three years. In fact foreign lenders are giving private banks at a lower rate and they are in turn flipping them to the government at a higher rate. In fact they seem to be more comfortable to lend to private banks for legal reasons among others. When the administration is strapped for cash it is not a bad strategy to go for shortterm borrowings, and to roll them over for a longer tenure when the fiscal situation improves in a few years’ time. This strategy is better than selling 30-year bonds at 12.5 percent at the longest end of the yield curve and generating a crisis in the bond markets and sending yields haywire as happened during the so-called bond scam.

However because the tenure is so short, next year’s rollovers are bunching up. In 2015 there were 1,091 million dollars of market borrowings coming for roll-over including a 500 million dollar sovereign bond. Next year there is no sovereign bond maturing, leaving a window to sell one. But even without a sovereign bond there are 1.24 billion dollars of floating rate bonds maturing, not counting any fresh one year debt that may be issued during the rest of 2015.

Central Bank Losses

● It is in this backdrop that the Central Bank is getting into very large swap arrangements with India. Former Deputy Governor W A Wijewardene has already raised a red flag about persistent central bank losses and also warned about the Central Bank of Philippines.

Instead of examining the warning, the Central Bank has come out with a denial. It must be said that when this columnist or Wijewardene or any other analysts issued warnings in the past, it was not done in the hope that the prediction will come true.

It is done with the hope action will be taken early to avert the problem. When Wijewardene was in the Central Bank, analysts and economists pointed out the danger of Sri Lanka going the path of Zimbabwe due to ‘Rata Perata’ and ‘Mahinda Chinthana’ fiscal and monetary policies. He did not argue with the critics.

It is well-known that the tight monetary targeting regime that was subsequently implemented was designed by Wijewardene. If not for that, the rupee would have been about 150 to 200 when the war intensified in 2009.

There is no point in saying central banks cannot go bust from losses quoting various people. The Central Bank of Philippines did and so did the Reserve Bank of Zimbabwe and most other hyper inflating banks.

A central bank makes losses mainly when the cost of sterilization (withdrawing liquidity from dollar purchases) is lower than the returns on its foreign reserves. When central banks make low profits or losses inflation is generally low.

A central bank makes large profits when there is inflation mostly because during those times it prints money and injects into the economy generating inflation or currency depreciation or both. It may also lose foreign reserves as Sri Lanka is doing now. When forex reserves are lost there is no longer any need to sterilize liquidity, hence the termination of term repos.

Profits of Misery

● A central bank also makes ‘profits’ when the currency depreciates (which is also inflation) and the value of its foreign reserves (net) goes up in domestic currency. So all large profits come from inflation. Even so one can argue that since a central bank can depreciate and inflate and print unlimited amounts of money, it can impoverish every saver, every wage earner and destroy the real value of every pension fund and remain solvent. The government also remains solvent by destroying the real value of domestic currency debt and making pensioners destitute.

This is what Sri Lanka was doing for many years. That is why Sri Lankans became poorer than say Maldivians or Singaporeans after independence. The root cause was the Central Bank which allowed the state to spend and default and spend and default in real terms.

In fact it is what Greece was doing for many years until it entered the Euro; entering the region by cooking its books. Why do Greek rulers want to get out of the Euro? So that it can default on the people through currency depreciation, and imposing ‘austerity’ on all, the rich and poor.

Instead Greek rulers are now forced to follow ‘state austerity’ but people’s bank deposits will retain their value. A 20 percent devaluation of any proposed ‘New Drachma’ is not only a 20 percent cut in ongoing salaries and pension payments of all people in Greece, but also government debt on lifetime private savings in private banks. People don’t really understand all this and that is why they are protesting. Deadly peddlers of state spending like Paul Krugman, perhaps the most vocal pro-ruler and anti-poor economist alive now, do not help by supporting the high spending Greek rulers.A central bank however can harmlessly make profits from its foreign reserves without generating domestic inflation, just like a currency board does.

Borrowed Reserves

Borrowed Reserves

● The Philippines Central Bank made losses also from giving cheap printed money under various credit schemes to ‘priority areas’ and sterilizing them at a higher rate like in Zimbabwe.

Mercifully during the time of Governor A S Jayewardene these Central Bank refinance schemes were stopped, though a small scheme is in operation dating from the tsunami and post war.

But Sri Lanka’s Central Bank has over 100 billion rupees of ‘provisional advances’ which are not just advanced at a low rate but at zero interest which it has to sterilize at the repo rate. Even this year about 9 billion rupees had been given. As part of a future Central Bank reform, the practice of giving interest free advances have to stop and existing advances have to be converted to Treasury bills, which can sold down.

The other most deadly source of losses at the Philippines Central Bank was its forex obligations. It had given forex cover through swaps to domestic banks and corporations to borrow abroad (sounds familiar?) and then it had taken central bank swaps.

By 1984, the Philippines central bank’s external liabilities had ballooned to 152 billion Pesos from 89.7 billion a year earlier. Its foreign assets rose to 17.6 billion from 12.1 billion. In 1984 the Philippines Central Bank lost 27 billion pesos, with 14 billion pesos lost on swaps and 5.3 billion pesos on forward cover. What this meant was that when the Peso depreciated, it no longer made profits because it lost on the swap.

This is the danger to the central bank. While it can always get out of local currency obligations by printing away and imposing losses on the general population it cannot do the same thing for dollar obligations. Sri Lanka’s reserves are not negative yet. But if 1.5 billion dollars are borrowed and spent on currency defence or repayments of foreign loans, then it can get partway there.Though some economists and even the IMF said the central bank had ‘borrowed reserves’ when Templeton funds bought a billion dollars of government bonds in 2009 it was not correct representation of actual events. The Central Bank ‘bought’ the dollars fair and then sold down Treasury bills to kill the liquidity.

It was the government that borrowed. The Central Bank had no liability. It bought the dollars by creating its rupee liquidity which was a noninterest bearing perpetual liability. It then sterilized the liquidity by selling down interest bearing Treasury bills that were bought originally to generate the 2008/2009 BOP crisis.

But when the Central Bank borrows from others like the RBI, its own balance sheet is at stake.

All of this goes to show that fiscal and monetary errors Sri Lanka did in the 1980s cannot be done in the same way now. Due to the heavy external borrowings both by the state and now by the Central Bank, it will not be able to get away with pro-ruler policy as easily as it did before.

Mulberry Bush

● Other matters remain the same. The problem with Sri Lanka’s central bank is that it never allows rates to go up in time, but intervenes in credit markets to create a bigger crisis, higher inflation and also currency depreciation either due to its own errors or due to fiscal dominance. To the recollection of this columnist the only time the Central Bank pre-emptively raised interest rates was around 1995 under A S Jayawardene (who was Treasury Secretary and then Central Bank Governor) following a desperately populist budget of the losing administration.

Now that all the term repo deals are ended excess liquidity should have been down to 17 billion rupees. Instead excess liquidity is at 83 billion rupees with 65 billion rupees in Treasuries bought by the bank.If the Central Bank’s open market operations were done correctly this liquidity should have been injected at the reverse repo rate of 7.5 percent overnight. Instead of which T-bills are being bought outright presumably at 6.2 percent or lower in a quantity easing exercise.

It makes nonsense of the policy rates. In the November 2014 The Price Signal by Bellwether, this column, warned that liquidity will run out and Sri Lanka will lose the reserves represented by the liquidity as the dam built by term repos was porous. It has now come to pass. “It should watch credit, watch foreign reserves and the exchange rate and refrain from keeping rates down when excess liquidity runs out,” the column said.

The Central Bank as usual is doing the opposite. In April it cut rates. But at least it is defending the rupee, which is the only option. With all the newly injected liquidity floating about, and the credit pressure, the rupee will have to be defended at the new level.

More rate cuts are on the way, apparently because inflation is low. Well what else is new?