The current financial climate is ideal for asset bubbles as the economy expands rapidly and credit grows in step, following the end of a quarter century long conflict. The cost of living is falling, almost everyone has a job and interest rates have declined to record lows. The country is in an upbeat mood about the future.

People’s and private sector expectations for the future rise rapidly during periods of high growth. People aspire for larger homes, vehicles and to consume more. Firms expect to supply the growing demand by expanding. Because they are now more optimistic, businesses and individuals will shed many of their inhibitions about debt.

The economic downside of confidence-driven borrowing is that it drives asset prices up. The cost of everything from homes, used cars and listed stocks rise when leverage increases demand for these assets. Considering the relative inexperience of Sri Lankan households and private firms with prolonged low interest rates, the likelihood they will bid up asset prices to bubble territory is very real.

The economic downside of confidence-driven borrowing is that it drives asset prices up. The cost of everything from homes, used cars and listed stocks rise when leverage increases demand for these assets. Considering the relative inexperience of Sri Lankan households and private firms with prolonged low interest rates, the likelihood they will bid up asset prices to bubble territory is very real.

When they pop, asset bubbles expose old shenanigans and encourage new ones, another likely outcome at some of Sri Lanka’s weak, ill-governed subprime lending firms. Faced with rising dud loans and tightening margins, owners and managers will gamble for salvation, taking even greater risks and speculative bets. They will conceal non-performing loans in the expectation that the prices of assets backing them will somehow recover, that these loans can somehow be packaged as a security and sold, or in the expectation the financial firm itself can be sold while the muck remains hidden.

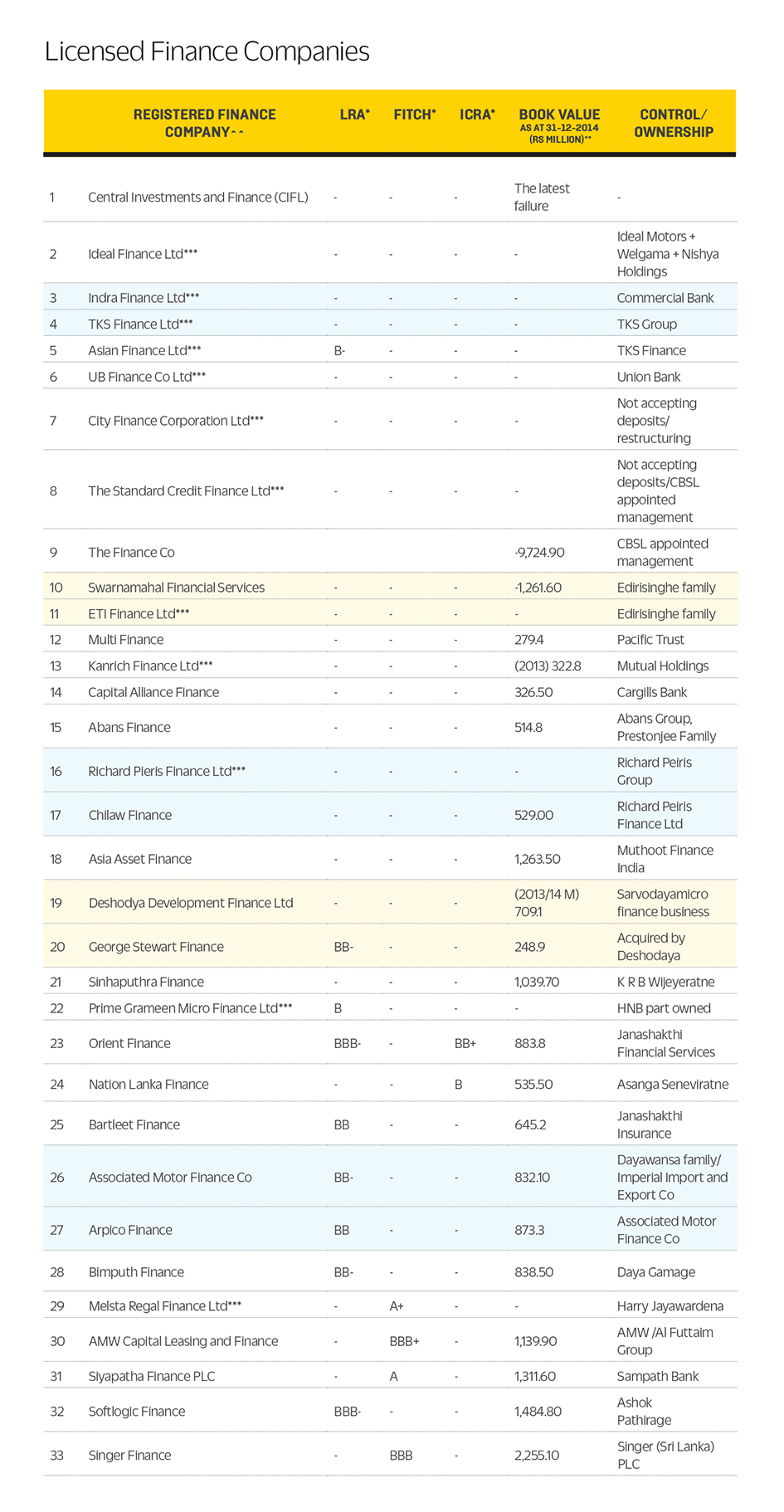

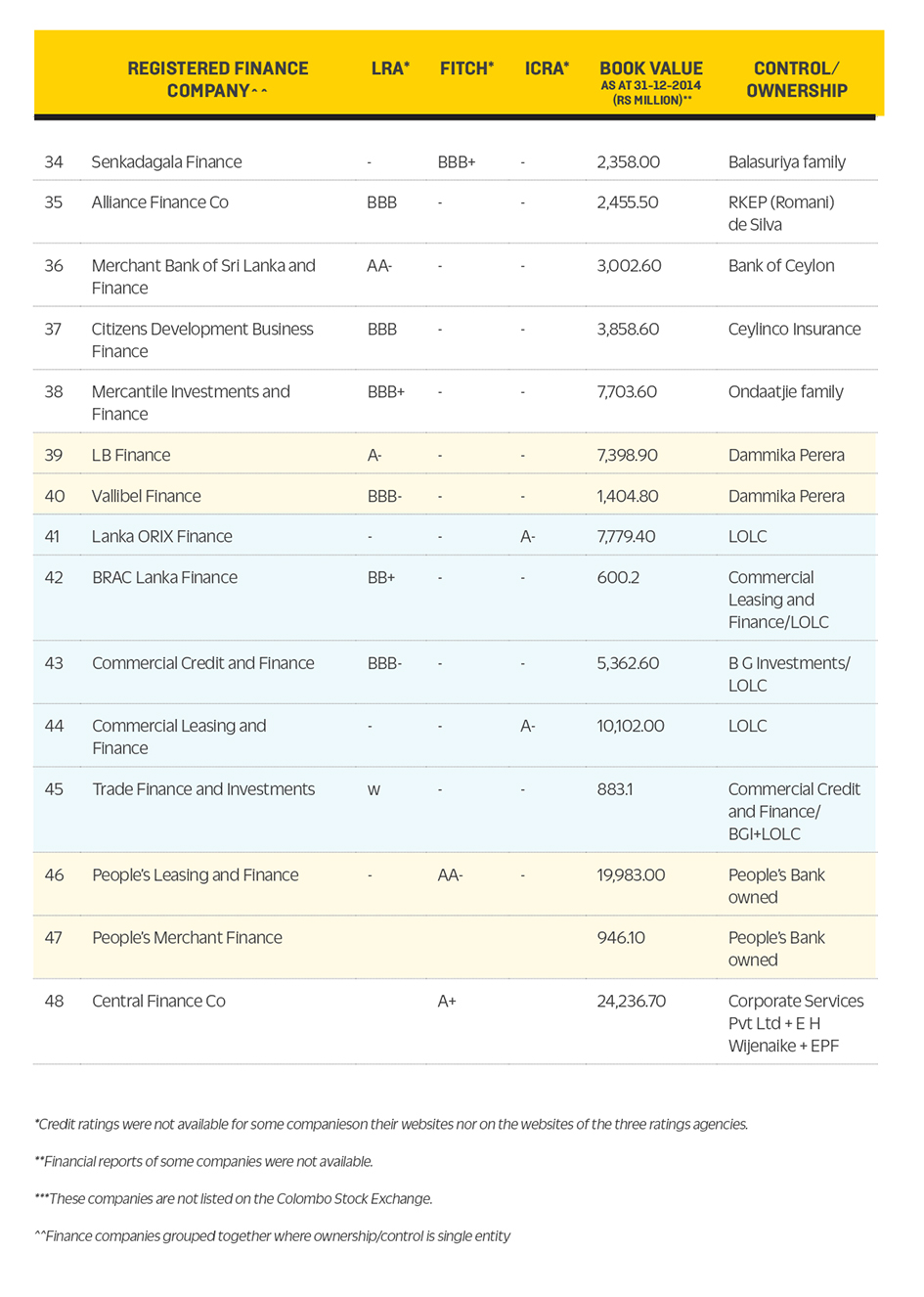

Many small subprime lending firms, commonly referred to as finance companies or Licensed Finance Companies (LFC), are badly managed and have a chilling disregard or good governance. The Central Bank – which regulates the sector – has, as a result, announced a policy of consolidation that will result in the weakest players being absorbed by bigger finance companies and commercial banks or the weak firms merging with each other to form larger, better capitalized finance companies.

Some small finance companies are concealing large nonperforming loan portfolios according to directors, chief executives, senior managers and analysts who spoke to Echelon. Due to the sensitivity of their revelations to firms and because they were not authorized to speak to journalists, those who granted interviews requested anonymity.

Trust underlies any financial system. Depositors – the major industry funding source – must have the confidence that their savings are safe. Undermining this confidence can lead to industry wide crisis. A financial sector firm’s fate is sealed if it has to block withdrawals.

Conditions that erode trust already exist. A third of the 48 registered finance companies aren’t transparent with their financial performance, 19 of them haven’t published a credit rating. Two finance companies have a negative net worth, two firms are not accepting deposits as they are restructuring and another, CIFL – where massive fraud is alleged – is being unraveled in court.

The finance company’s websites, websites of the three credit rating agencies nor Echelon’s team visiting the head offices of these 19 firms were able to figure if they currently had a credit rating.

Central bank has been vague about finance company non-compliance with directions, guidelines, circulars and regulations. Proposing acquisitions and mergers (consolidation) among finance companies and with banks in January 2014, the Central Bank observed that 38 non-bank financial institutions (which also includes a few leasing companies) had weak compliance with regulatory directions.

The murkiness and the risks seem to have alarmed the regulator. In 2014 it proposed consolidation in the financial sector and reducing the number of finance companies – by

The murkiness and the risks seem to have alarmed the regulator. In 2014 it proposed consolidation in the financial sector and reducing the number of finance companies – by